The $13 Billion Mirage: How China’s Industrial Pledges Could Trigger Western Trade Sanctions

TL;DR

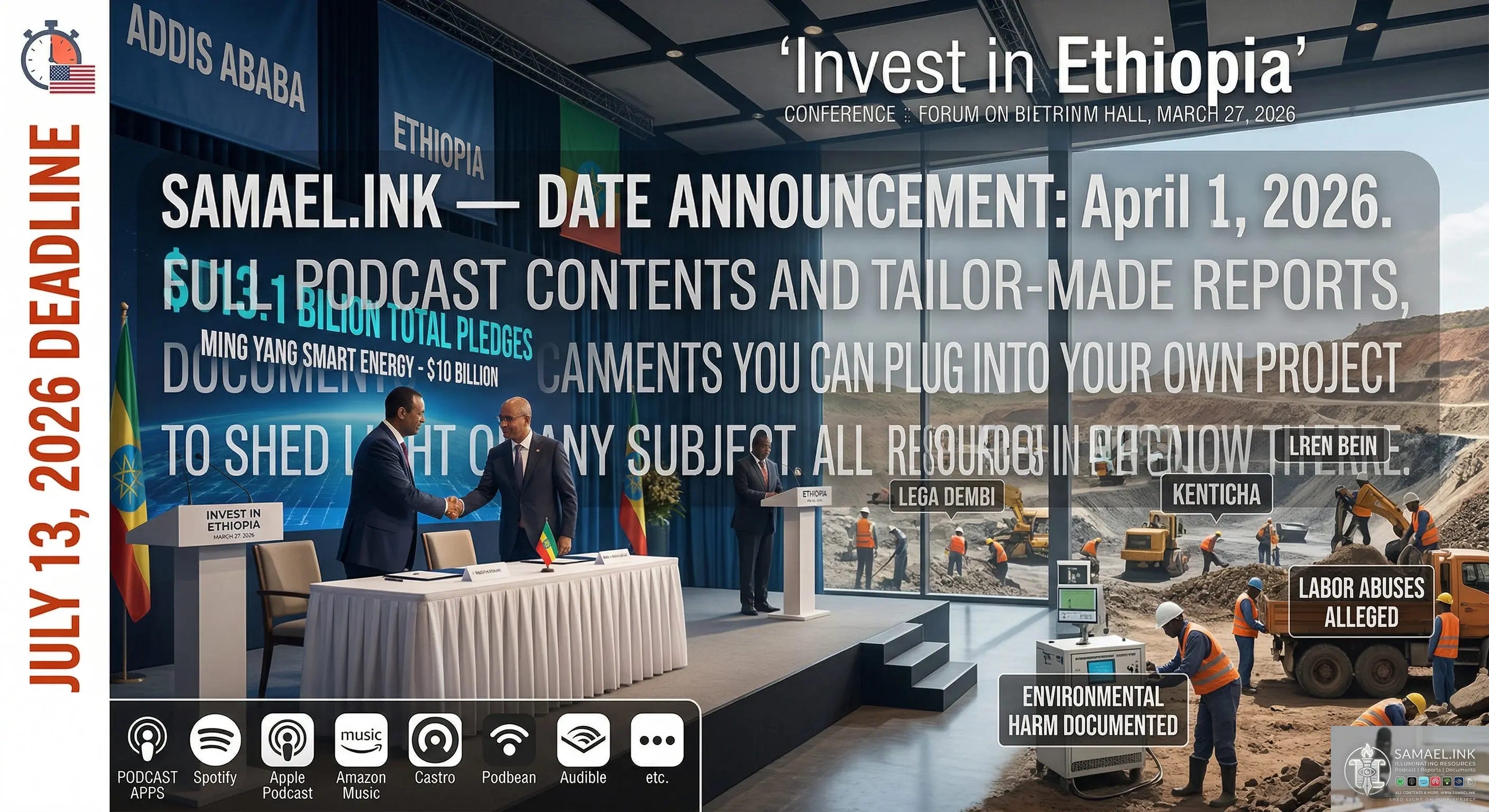

Ethiopia’s March 27 Invest in Ethiopia forum produced a headline $13.1 billion in industrial pledges—dominated by a $10 billion commitment from Ming Yang Smart Energy—just as mounting evidence of environmental harm and labor abuses in mining regions raises the real prospect that U.S. trade measures on processed critical minerals and labor practices will close Western markets by the July 13, 2026 deadline. Without independent environmental and chain-of-custody audits, large parts of Ethiopia’s exportable mineral supply risk exclusion or steep trade penalties under imminent Section 232/301 actions.

Background and context

The Addis Ababa investment announcements aim to rapidly industrialize processing capacity—green ammonia, electrical equipment, and mineral processing—to capture more value domestically. That strategy reads as a hedge against potential Western market restrictions: build processing inside Ethiopia to claim local value addition and reduce dependence on raw‑export markets. But the timing coincides with intensified U.S. reviews of critical minerals supply chains and labor‑related trade remedies, creating a narrow window to demonstrate compliance with environmental, labor, and traceability standards.

Investment Wave: What $13.1 billion actually means

Composition: Roughly $10B from Ming Yang Smart Energy Group targeting green ammonia and electrical manufacturing; remaining commitments from Indian, Polish, Singaporean, and Kenyan firms focused on downstream manufacturing and logistics.

Strategic intent: These deals appear structured to lock in long‑term industrial footprints—power infrastructure, industrial zones, and processing hubs—that would integrate Chinese capital and suppliers into Ethiopia’s critical‑mineral value chain.

Practical risk: Pledges often include multi‑year MOUs and phased financing; many are conditional on regulatory clarity, land access, and security—factors complicated by local conflict and reputational scrutiny.

Human and environmental counterweight: Kenticha and Lega Dembi

Lega Dembi (Guji Zone): Ongoing contamination reports show elevated cadmium, mercury, and cyanide exposures, with documented adverse reproductive and developmental health outcomes. The persistence of these issues undermines claims of “green” processing and will be potent evidence in any environmental penalty assessment.

Kenticha (lithium): Despite substantial lithium resources, Kenticha faces legal ambiguity, opaque contractual arrangements, and absence of independent environmental and social impact assessments (ESIAs). That opacity makes any downstream product from the site highly vulnerable to traceability challenges and “dirty mineral” labeling under import rules.

The July Wall: How U.S. trade tools apply

Section 232 (Processed Critical Minerals/PCMDP): The Commerce Department’s review targets processed minerals whose processing occurs under undue influence of strategic rivals. If Chinese‑linked processing is deemed to create supply‑chain risk, imports can face Minimum Import Prices (MIPs), quotas, or exclusion from strategic stockpiles such as Project Vault. Processed Ethiopian lithium or tantalum routed through Chinese capital structures is at high risk.

Section 301 (Labor/Unfair Trade): The USTR’s labor nexus probe targets state‑linked military‑mining ties and labor abuses (unpaid wages, forced labor indicators). Findings here can trigger tariffs or remedial measures on specific product lines or companies.

Timing and consequence: The July 13 reporting and subsequent determinations create an operational deadline: without robust, verifiable remediation and traceability, Ethiopian minerals may face immediate market barriers.

Breakdown of risks and likely outcomes

Traceability failure: No independent chain-of-custody audits → high likelihood of exclusion from U.S. critical‑mineral procurement and private Western buyers seeking Clean Chain assurances.

Environmental penalty: Documented contamination and public health impacts → basis for environmental adjustments under Section 232 and reputational bans by major buyers.

Labor sanctions: Evidence of unpaid wages and opaque contractor structures → triggers for Section 301 punitive tariffs.

Investment façade risk: Paper pledges that depend on contested land, insecure supply chains, or conditional financing may not translate into durable industrial capacity before the July deadline.

Practical implications for buyers and financiers

Western buyers will likely demand verifiable traceability and third‑party certification before offtake deals; financiers will require stronger environmental and social covenants in lending documentation.

Chinese‑backed projects without independent audits may find capital and offtake constrained to non‑U.S. markets, raising project viability questions.

Short‑term market distortions: opportunistic arbitrage could reroute supply to markets with lower human‑rights scrutiny, but that raises longer‑term pricing and insurance costs.

Limitations and uncertainties

The $13.1B figure reflects announced commitments; the pace and realization of funding, construction, and operationalization are uncertain and contingent on security, regulatory, and financing conditions.

U.S. determinations under Sections 232/301 depend on final agency findings, legal interpretations, and diplomatic interventions; outcomes are probable but not certain.

On‑the‑ground remediation timelines for heavy‑metal contamination are long and technically complex; quick fixes are unlikely to satisfy Western traceability expectations.

What was the headline investment announced at Invest in Ethiopia 2026?

— A total of $13.1 billion in new commitments, with about $10 billion pledged by Ming Yang Smart Energy Group for green ammonia and electrical equipment manufacturing.

Why does the Ming Yang pledge matter geopolitically?

— It ties major processing capacity to Chinese capital, potentially entrenching influence over power and industrial corridors that process critical minerals.

What are the main environmental concerns?

— Persistent contamination at Lega Dembi with mercury, cadmium, and cyanide linked to serious reproductive and developmental health harms.

Why is Kenticha particularly sensitive?

— Large lithium resources exist but the site lacks independent ESIAs and transparent governance, making downstream lithium vulnerable to “dirty mineral” designations.

What is the “July Wall”?

— The July 13, 2026 reporting window for U.S. Section 232/301 reviews that could impose MIPs, exclusions, or tariffs on minerals processed under suspect chains or linked to labor abuses.

How can Ethiopia avoid U.S. trade penalties?

— Implement immediate independent environmental audits, transparent chain‑of‑custody systems, labor/payroll audits, and secure Western certifications before the July deadline.

Will the $13.1B in pledges protect Ethiopia’s access to Western markets?

— Not by itself; without verifiable remediation and traceability, much of the pledged processing capacity could be deemed tainted and blocked from key Western markets.

What role can international partners play?

— Provide technical audits, certification frameworks, conditional financing linked to remediation, and diplomatic engagement to demonstrate compliance.

How certain are these trade‑restriction outcomes?

— They are plausible and time‑sensitive given current investigations, but final determinations depend on agency findings and possible diplomatic mitigation.